Third Quarter 2021 Market Insights

September 30, 2021

“Complexity is your enemy. Any fool can make something complicated. It is hard to keep things simple.”

– Richard Branson, Founder of the Virgin Group of companies

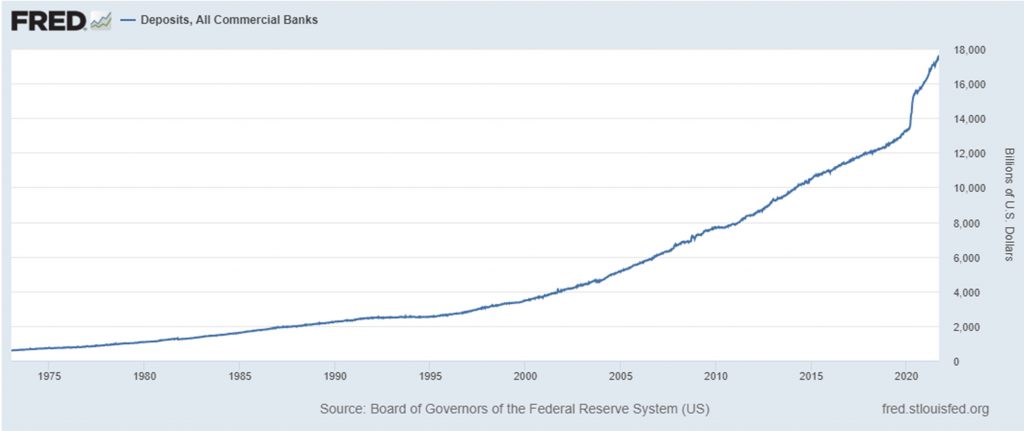

We don’t typically invest client funds in bank deposit products- and publicly traded bonds are certainly different in many respects than bank deposits- but we are facing a similar rate conundrum with the cash equivalent and fixed income segments of our client portfolios. Money market funds and T-Bills are generally yielding less than .10%. The rates being paid on U.S. Government bonds remain near historical lows, and it is unusual to find a yield exceeding 2% among Investment Grade Corporate bond offerings, even for maturities beyond 10 years. Looking outside the U.S., there continues to be greater than $13 trillion in negative-yielding worldwide debt, validating that at least some investors have not only accepted low-interest returns, but are even tolerating a reduced return of principal.