Overview of the critical tax related modifications impacting our clients in the 2018 tax year

As you think about the new tax legislation, officially known as the Tax Cuts and Jobs Act of 2017, remember most of the changes will NOT affect your 2017 tax returns to be filed over the course of the next few months. And, unless extended by Congress, most of the new provisions will expire at the end of 2025 with the law then reverting back to those in effect for 2017. However, there are several key components of the Act that likely will impact you directly or indirectly beginning in 2018:

- The corporate income tax rate was reduced to 21%, returning the U.S. to the realm of tax competitiveness with the rest of the developed world.

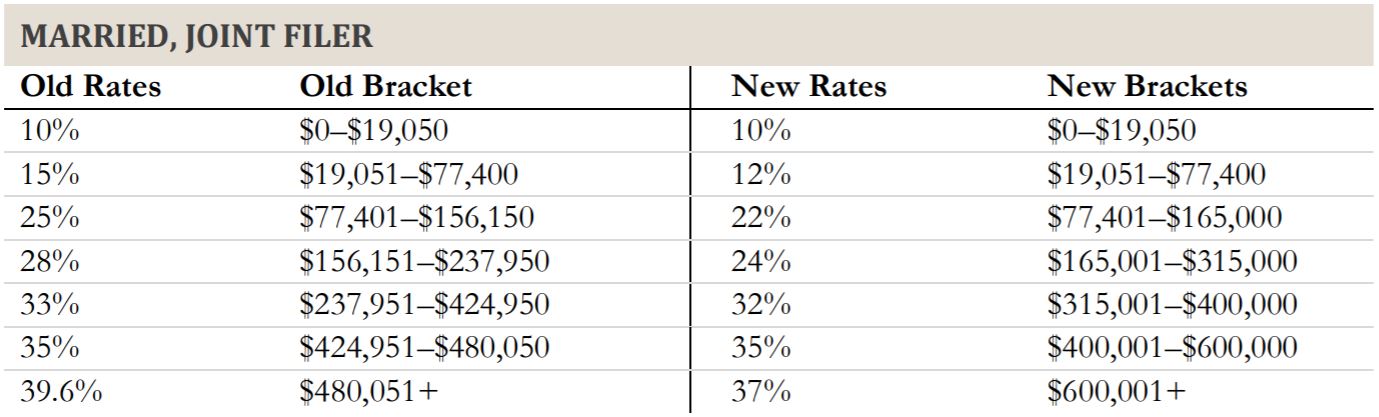

- Individual income tax brackets under the Act have generally higher income thresholds and lower rates, with rates now ranging from 10-37% (refer to chart below for Married Joint Filers, as an example). The Center for Tax Policy estimates the average marginal tax rate for individuals will decline by roughly 3.2%.

- The Act substantially increases the standard deduction. For married joint filers, the standard deduction will now be $24,000 (up from $12,700) and for single filers it will be $12,000 (up from $6,350 in 2017).

- For those who will still be able to itemize deductions, the Act limits the amount of deductible state and local property taxes, income taxes, or sales taxes paid to a cap of $10,000. Interest on existing or new home equity debt is no longer deductible under the Act. In addition, miscellaneous expenses (formerly considered to be deductible to the extent they exceeded an income threshold), such as moving expenses, tax preparation fees and investment management charges, will no longer be deductible.

- The threshold for deducting medical expenses for all taxpayers has declined from 10% of AGI to 7.5%.

- The Act does not change the treatment of existing mortgages, but mortgage interest beginning in 2018 will only be deductible for loan amounts up to $750,000 and only for a taxpayer’s principal and second residence.

- The Alternative Minimum Tax (AMT) did not get eliminated as was hoped. Instead, the non-married filer exemption was increased to $70,300 and the exemption for married filers increased to $109,400, with the exemption starting to be phased out at $1 million.

- 529 College Savings plans were expanded by the Act with the allowance of up to $10,000 per year to be used toward K-12 tuition expenses.

- The child tax credit was doubled by the Act from a current level of $1,000 to $2,000 per child. The increased credit is intended to offset the repeal of the personal exemption for dependents.

- Historically, alimony payments have been considered taxable income for the recipient, and the payor was able to deduct alimony as an expense. That will be grandfathered in for agreements executed before 2019. For those settled thereafter, the deduction is eliminated and payments will not have to be included in the taxable income of the recipient.

- Unearned income of children (think dividends and interest) along with earnings in UGMAs (Uniform Gift to Minors Account) above $2,100 will continue to be subject to income taxes – better known as the “Kiddie Tax.” However, in the past the Kiddie Tax was based on the parents’ marginal tax rate. Starting with 2018 returns, the Kiddie Tax for unearned income and capital gains in excess of $2,100 will be calculated using the highly progressive trust and estates rates (37% rate applied for all income above $12,500).

- Deductions for charitable cash contributions and certain private foundations are allowed for up to 60% of the AGI, versus 50% in 2017.

- The amount any person may transfer to another without gift tax consequences, also known as the annual gift tax exclusion, was raised by the Act to $15,000 per donee.

- As of January 1, 2018, the lifetime estate and gift tax exemption was increased from $5,490,000 to $11,200,000 per individual. Married couples may now transfer up to $22 million free from estate or gift tax.

We hope you find this very broad brush summary of the new law to be helpful. We’ve only touched the surface, but trust if one of our bullet points strikes a chord, you will call us or seek advice from your tax professional.