John M. Suddeth, Jr., CFA

As we turn the page to 2020, practically every investor on the planet wants to know how the U.S. election scoreboard will look come the middle of November. We admittedly lack the foresight of the Great and Powerful Oz but can still take a page from Frank Baum’s wizardly wisdom and analyze past election year experiences as a glimpse of what might be in store. Going back to 1928, the S&P 500 Index has advanced in 16 of the past 22 presidential election years.1 At 72%, those odds are attractive but certainly not fool proof. As we zero in on what might fuel corporate earnings growth, we can envision an economic palette where abundant jobs, shockingly low deposit rates, and a surge of U.S. political spending could all prove supportive. Peering past November, history tells us stock market success increases substantially in a year when the incumbent party stays put, enjoying an average increase of 11% versus only 0.3% when the incumbent is ousted. The obvious caveat to that range of outcomes is timing, as elections usually aren’t finalized until 90% of the year is past. Given the unusual state of U.S. politics, we urge investors to maintain ample liquid flexibility and to expect “statistical divergences” (as a euphemism for risk and volatility) in 2020. Sitting on the sidelines may appear compelling, but beware of trying to perfectly time exit and entry as the rapidity of market swings could be ferocious given the stakes. Ultimately, it will likely be the bold, those who can establish and maintain positions in a period of panic, who stand to reap any outsized rewards.

Having mentioned risk, few people understand it as intently as Warren Buffett. He has made a career, and a fortune, out of pricing all kinds of risk via his Berkshire Hathaway reinsurance company. We noted Buffett’s recent candor in talking about cyber risk, an expanding category for commercial insurers that was barely on the underwriting radar just a decade ago.2 Buffett stated “Frankly, I don’t think we or anybody else really knows what they’re doing when writing cyber,” and anyone who says they fully understand cyber risk pricing “is kidding themselves.”

Carnival cruise line is expected to deliver their first North American-based cruise ship powered by liquified natural gas (LNG). This announcement stood out as another example of a mature company’s continuing creative evolution. In addition to lowering their fuel cost from an apparent abundant supply, Carnival is responding to the market’s push for a less carbon-intensive footprint. This LNG powered vessel, the Mardi Gras, will be their largest ship ever holding 5200 passengers, employing 1745 crew, and featuring a spectacular upper deck roller coaster. At a cost of over $1.3 billion, the 18-month long build process employed thousands and will continue to employ thousands for years to come. As we enter the new decade, it is important to be reminded that businesses need to remain dynamic to maintain relevance. It is not just the Ubers and Amazons of the world who are uniquely engaged in forging new paths into tomorrow.

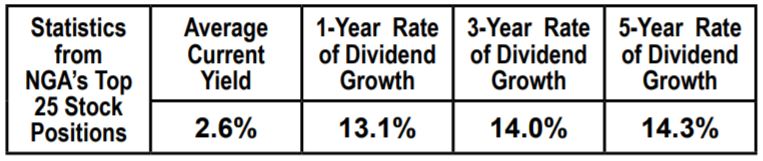

Inflation, paying more for the same item or service from a prior period, has fallen out of the spotlight in recent years. In moderation, inflation is actually a good economic force and provides a backdrop for higher savings rates and earnings growth. As business owners with a bent to maintaining profitability, we have sensitivity to rising, or inflationary, operating expenses and have been experiencing higher costs, practically across the spectrum of our business activities: leasing rates for office space, upgrades for technology, cost of research travel, insurance premiums, etc… Name the expense, and they all seem higher than in previous years. The “price of life,” so to speak, has been moving up even as interest rates have been falling. We are therefore not surprised by the recently reported “official” U.S. inflation rate, which came in at a 2.1% annualized rate.3 This figure is above the levels of the past few years. Inflation around the developed world has been barely present, at least by Central Bank standards, yet on a day to day basis it couldn’t be missed. Thinking of the forward impact, cyber risk policies will probably cost more, Disney’s park passes have had only one trajectory (up), and we have little doubt that a ticket to ride a cruise ship with a roller coaster will come at a premium to an older vessel without one. This reality of a perpetually rising cost of life for our clients prompted us to analyze and quantify the multi-year dividend growth rates, our philosophical investment antidote to inflation, for our top 25 holdings, which is shown below:

Finally, as the dynamics of an election year unfold, we fully expect to have days in the financial markets that will resemble Dorothy’s farmhouse in a Kansas cyclone: spinning out of control, not sure exactly what awaits on the landing. In a world of over 7.7 billion people, we take comfort in the consistency of human creativity, the capacity for technological innovations, and the meritocratic work ethics that are all naturally displayed through capitalism, despite its imperfections. Within that complex, one of our important roles is to identify and invest client capital into forward-thinking companies that bring enthusiasm into the new decade and have the proven financial capacity to weather the inevitable economic and political storms.