Reporting by Isaac Codrey, CFA

Citius – Altius – Fortius

With every country hunkering down and tightening up its borders, global travel ceased, making it impossible for these global events to be held. The travel halt also impacted our own business as 2020 was the first year in which we did not perform any international research trips. (Thankfully, that was the only major disruption to our business, but it is one we look forward to ending in the near future.) All told, U.S. travel spending declined an unprecedented 42% in 2020 according to the U.S. Travel Association. Even more precipitous were the 70% decline in travel business spending and 76% decline in international travel spending. It’s no wonder those dependent on these travel-related flows have financially suffered.

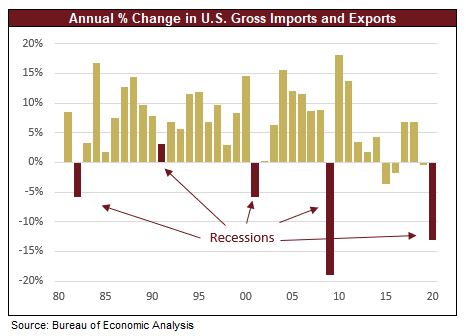

While the movement of goods did not face the same stringent restrictions as the movement of people, the global supply chain has been trapped in its own logistical quagmire. What started off with factory shutdowns in China during the first quarter of 2020 proliferated across the globe as most governments forced economies into lockdown. The knock-on effects are still reverberating. The global semiconductor chip supply shortage (mostly manufactured in Asia) that is forcing U.S. automakers to shut down manufacturing lines because they don’t have all the parts necessary to the roll the car off the line is but one visible example of shortages that are plentiful.

Therefore, as investors, our belief in the global opportunity set has not wavered. If anything, this period has helped us unearth hidden values not only in our tried-and-true developed markets, but also in new markets such as Malaysia. We continue to believe in the benefits of owning foreign companies and receiving dividends in foreign currencies. In fact, those dividends, domestic and foreign, are our main combatant against the number one perceived risk in today’s market—inflation.

After more than a decade of dormant inflationary pressures, inflation is starting to rear its ugly head. The prices that consumers paid for goods and services increased 5% from May 2020 to May 2021. Admittedly, comparing this year to last year seems a bit silly. Most, if not all, economic figures (e.g. GDP, employment, prices) are likely to exhibit eye-popping growth over the past year, but there is more to the story than this so called low base effect.

Inflation is something we anticipate and factor into our personalized asset selection process on an on-going basis—not just when the threat is looming. It begins with asset allocation and continues through the individual security selection. The nature of our very investment criteria is such that our client portfolios are constructed strategically to counterbalance a higher inflationary environment. Our philosophy for each major asset class (Cash, Fixed Income, and Equity) is tailored to deal with this risk, but ultimately, equities and their consistently growing dividends are our best combatant in the fight against inflation.

Although inflation has been quiet for decades, many of the companies in which we invest can draw upon their experiences from the 70’s. Even for those companies which have yet to compete against such a formidable adversary, the playbook will be the same. In typical high-inflation environments, a short-term shock hits the bottom line of income statements as the cost of goods and/or wages eat into profit margins. Ultimately, robust companies discover ways to either pass those costs onto customers via higher prices on their goods or services, or they reduce their own cost structure via increased efficiencies. In essence, we remain confident that the companies in which we invest will handle inflationary pressures in stride once again and will still be able to grow their revenues and earnings through the economic cycle. Earnings growth is typically a good recipe for appreciating stock prices, but more importantly, it is a great recipe for increasing dividends. The companies in which we invest have historically increased their dividends by an average of 6-8% a year, and we expect this trend to continue, even during inflationary periods. What better way to combat inflation than to have your dividend income growing at a pace that is faster than the expected increase in the cost to live?

Ultimately, it is our goal to identify companies that adapt to various challenges (e.g. inflation) —companies that will grow faster, push their dividends higher, and leave their shareholders in a stronger financial position. With the much-anticipated summer Olympics right around the corner, we leave you with this: we will continue to invest in companies that we believe will live up to the Olympic Motto “Citius, Altius, Fortius” – Latin for “Faster, Higher, Stronger.”